IFRS presentation practice differences: a European problem revealed and amplified by digital reporting

One standard, but a flexible standard

Investors and creditors need to understand a company’s financial position and financial performance, with a high degree of confidence, before they can invest in the company.

When a user of financial statements is familiar with a specific set of accounting standards, it can be a serious challenge to properly understand financial statements built in reference to other accounting standards. The vocabulary is often very similar but its meaning can change significantly.

This is even more pronounced when the other accounting standards are in a foreign language. A company building their financial statements in a non-English language, then translating them to English will often try to use common accounting terms for their translation, even though the translation may be only approximate.

Given the above, to foster investment across borders in Europe (even beyond the EU), companies listed in regulated markets report their consolidated financial statements using the same accounting standards: the International Financial Reporting Standards (IFRS).

Because of the nature of international consolidation of companies and subsidiaries across all activities, it was decided that the IFRS would be principle-based. This means that the IFRS does not prescribe an exact format for the financial statements. Some minimum requirements exist, but a lot of flexibility is provided, as long as the preparer adheres to the principles the standards state.

In the balance sheet

IAS 1 Presentation of Financial Statements (as well as its successor, IFRS 18) is the standard that describes the structure of the primary financial statements.

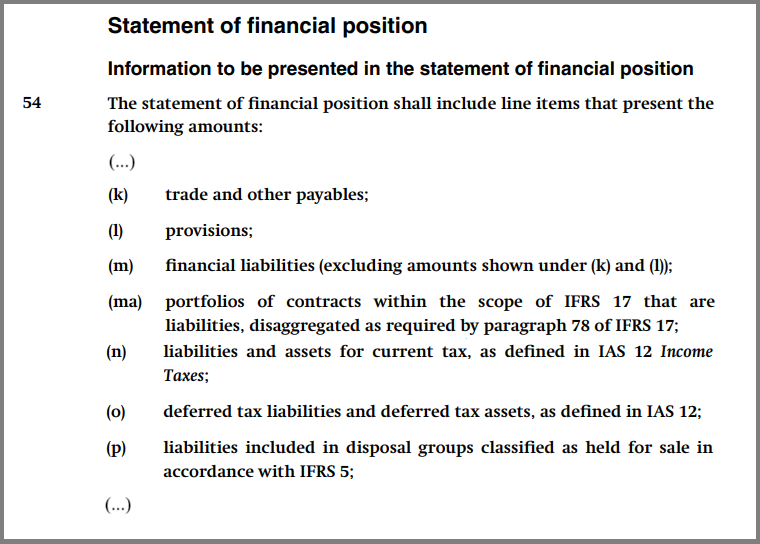

It notably specifies distinct categories of assets or liabilities to be presented within line items in the balance sheet:

Excerpt of IAS 1 paragraph 54, amounts to be presented within the liabilities of the company

This doesn’t mean that companies need to present exactly these amounts each on a separate line. Companies can aggregate or disaggregate these amounts in the way they judge best for the understanding of their liabilities.

As a result, since the categories of assets and liabilities relevant to a company’s activities and specific position vary a lot, so do the presentations of their balance sheet. Yet, these balance sheets can remain understandable.

Indeed, while this allows for a lot of flexibility in presentation, to keep the statements understandable, the IFRS include some clarity requirements. In particular, additional subtotals are required to be ‘labelled in a manner that makes the line items that constitute the subtotal clear and understandable’ [IAS 1 paragraph 55A(b)].

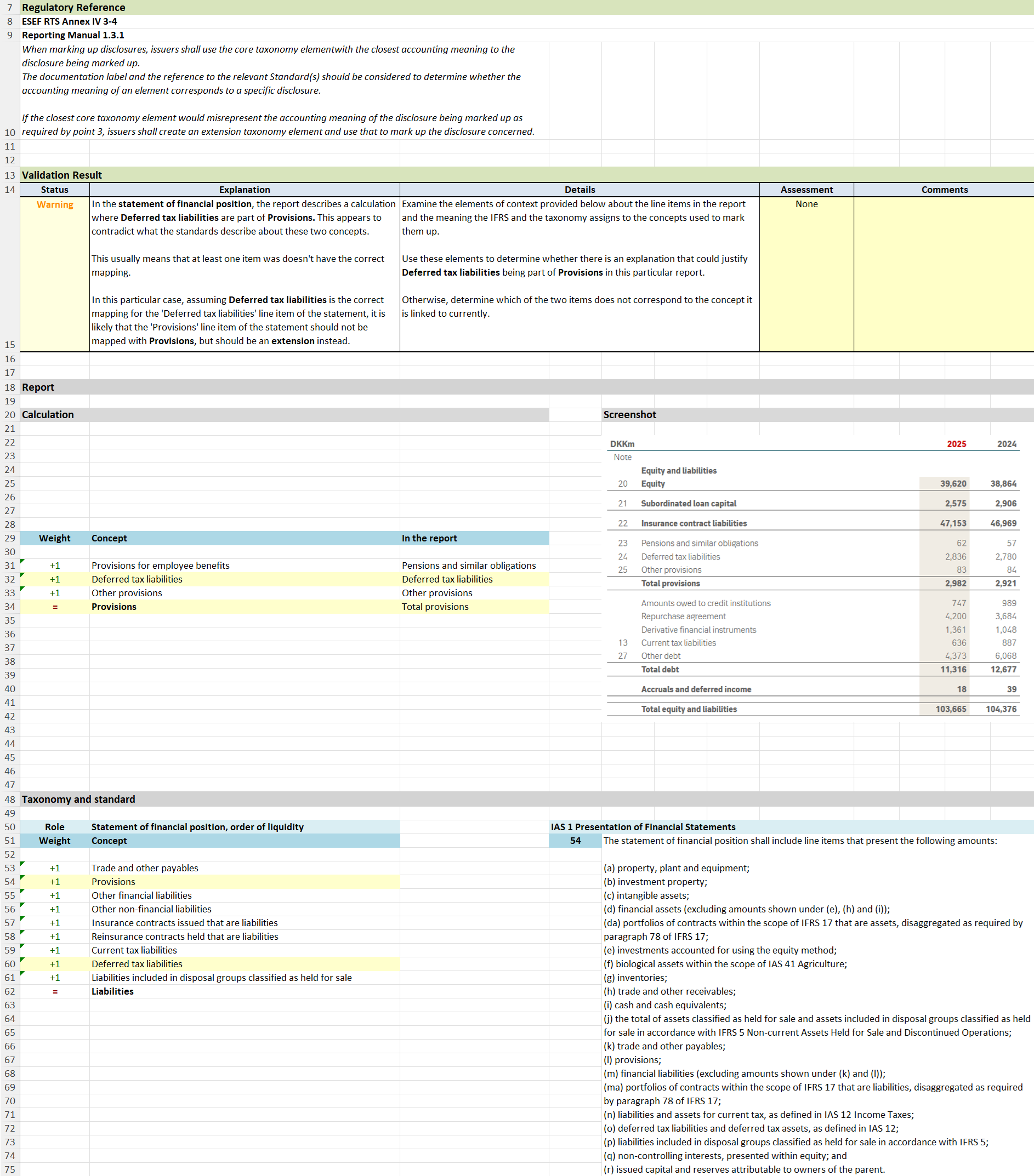

For instance, it could be considered incorrect to label a line item ‘Provisions’ if it contains significant items other than provisions, or if part of the provisions are included in a non-obvious fashion in another line item.

A Danish insurance company: Tryg

The presentation choice

Tryg A/S is, as it advertises, one of the largest non-life insurance companies in Scandinavia. It is listed on Nasdaq Copenhagen.

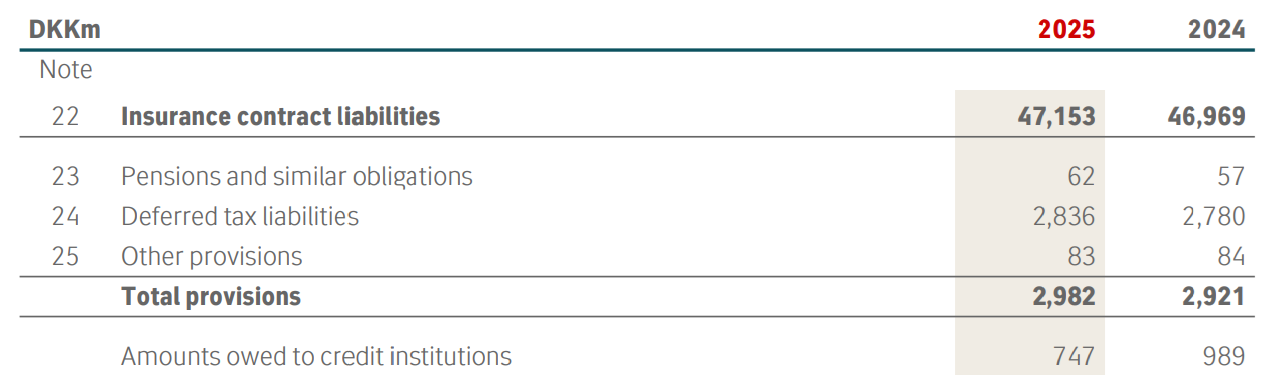

This is the liabilities section in the balance sheet of their recent consolidated financial statements:

Excerpt of the liabilities section in the balance sheet of the Tryg A/S Annual Report 2025

One can notably see that Tryg presents a ‘Total provisions’ subtotal in which the major component is ‘Deferred tax liabilities’.

Importantly, as quoted before, in IFRS, ‘provisions’ and ‘deferred tax liabilities’ are completely distinct items. They are respectively given precise definitions in their own respective standards, IAS 37 and IAS 12.

As a consequence, the line labelled as ‘Total provisions’ does not actually represent provisions. In fact, very little of the amount presented actually consists of provisions.

Origin

The reason behind this presentation choice can be traced to the way the consolidated financial statements were created. Companies often start from their local accounting standards, then ‘translate’ the presentation into what they deem consistent with IFRS as they consolidate subsidiaries from possibly other countries.

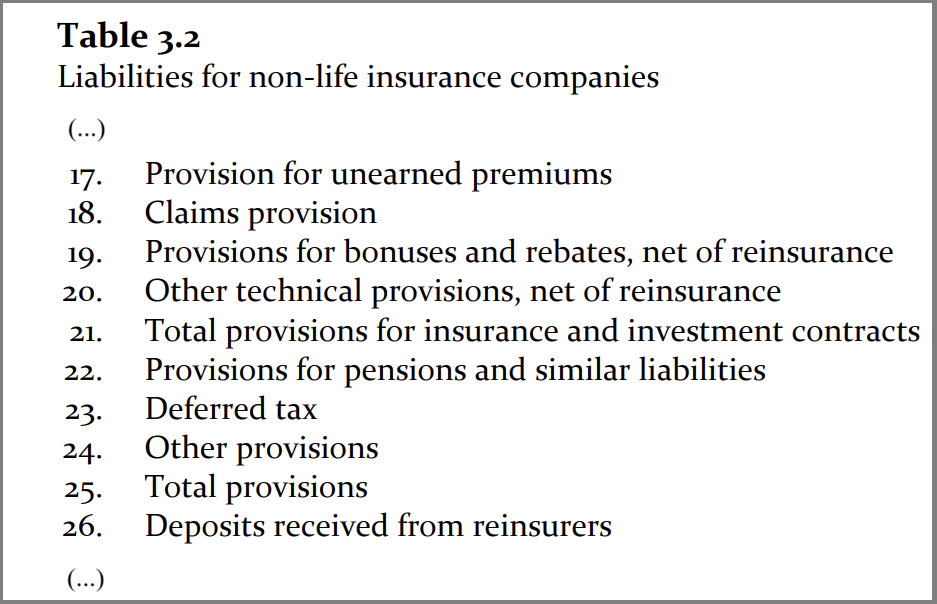

It is reasonable to suggest that this is exactly what happens with Tryg. Indeed, in the Danish financial statutory balance sheet for non-life insurers, here are the line items in liabilities:

As one can see, there is a notion in that balance sheet, translated as ‘provisions’, that does include deferred tax liabilities.

That does not mean that Danish accountants actually think this matched provisions perfectly. Instead, they define their own notion ‘hensatte forpligtelser’, to generally represent amounts representing uncertain financial obligations. When a translation into English was required, this notion was translated into ‘provisions’, which was deemed a close enough approximation.

Compliance

If the line labelled ‘total provisions’ mostly does not contain provisions, is this compliant then, as regards the clarity requirements in IAS 1 55A we quoted earlier? Ultimately… ‘yes’, as for almost all consolidated financial statements, the financial statements of Tryg are subject to audit, and auditors either decided that this was compliant, or that this was not material enough.

The most likely reason is that the clarity was judged considering the line items as a group. Even though the line item is labelled ‘total provisions’ and provisions do not include deferred tax liabilities, the presentation makes it clear here that the subtotal does include deferred tax liabilities. Therefore, it can be argued that one could easily realise that the subtotal does not actually correspond to provisions.

It is compliant, then, yes. But is it misleading?

Yes, without a doubt, and as a matter of fact, the proof comes from the company itself, in the digital version of their consolidated statements they publish.

The electronic mark-up

As has been the case since 2021, Tryg is required to publish its report in an electronic format (ESEF).

The main feature of this electronic format is a requirement to mark-up the monetary amounts in the primary financial statements with metadata that clarifies how precisely the amounts relate to terms defined in the standards, or to common practice terms.

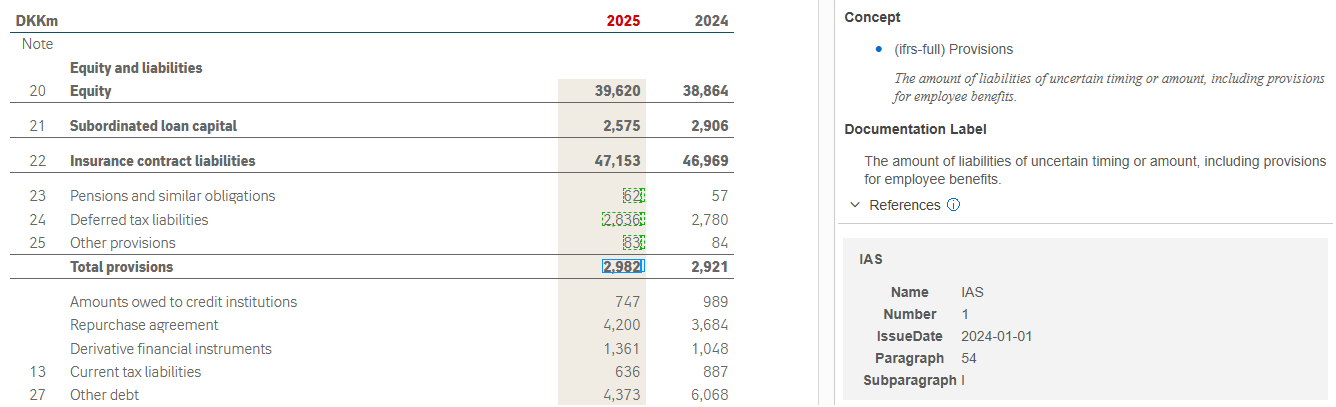

The electronic format can be consumed by tools to allow automated or manual inspection of this information:

The mark-up of the Total provisions as declared by Tryg itself, in a ‘viewer’ tool that shows the marked-up metadata

As shown above, when Tryg itself marked up the amount next to ‘Total provisions’, it declared it to correspond to the standard definition of ‘provisions’ in IFRS, i.e. to the item described in IAS 1.54(l).

This of course has technical consequences when it comes to the consumption of the data through electronic means.

But more importantly, if Tryg itself does not identify the mismatch between the label and the standard definition, it seems difficult to argue that readers are not likely to be misled by the presentation and that it is clear enough…

It is of course not the intention of Tryg to mislead readers in any way. As we explained above, this is simply a consequence of the way the consolidated statements were prepared, and maybe of a mis-appreciation of the ease of users to deal with approximate labels.

To the contrary, it can be very difficult after years of established habits to realise that the presentation a company is accustomed to is problematic; and that is all the more true when the origin is rooted in local accounting, as the closest peers might not be able to highlight the issue either.

That is why Rift Technologies endeavours to provide companies and their reporting stakeholders with the means to detect how their presentation might be unintentionally unclear.

How to detect and solve

The ‘ESEF’ electronic format amplifies the importance of properly identifying the meaning of each line in the financial statements. This also means we can use it to detect issues similar to the one in Tryg’s report.

To do so, we may use a resource the IFRS Foundation prepares and maintains: an ‘IFRS Accounting Taxonomy’ whose primary purpose is to enable digital reporting, that describes relations of concepts with the standards and with each other.

This taxonomy can be used to enable an automated analysis of a set of financial statements and an assessment of their alignment with the standards.

The development of such analysis tools requires a dual expertise, in both technological and accounting aspects, that few companies combine. Fortunately, Rift Technologies does, and already provides software with such capabilities.

In particular, if you want to know whether your report or a report you work on contains any such issues, you may use the Rift Technologies validation engine. It is able to not only flag inconsistencies between the mark-up and the standards, but also provides a clear view of what exactly is inconsistent and what the standards imply.

Example output from the Rift validation engine of the Tryg Annual Report 2025

Do you want to know more about these capabilities in the Rift validation engine, or about its other features? Don’t hesitate to contact us, we will be happy to discuss!