Consistency between European sustainability reporting and other EU frameworks, year 2

Reminder: non-recycled waste, year 1

Last year, the first reports disclosing sustainability statements according to the European Sustainability Reporting Standards (ESRS) were published. I browsed many of them, eager to see whether we could finally have a reliable source of data that would notably enable sustainable finance users to gather the information necessary to fill the reports required by Sustainable Finance Disclosure Regulation (SFDR), designed to let the general public know, in a comparable fashion, the degree of sustainability of the financial products they invest in.

One key concern of mine was that, after EFRAG (the standard setter for the ESRS) first proposed that the data required for other EU requirements would be mandatory disclosures when their topic was material, the European Commission had the standards amended to make everything subject to judgement.

However, as I started reading the published sustainability statements, I realised that there was a much bigger issue I (naively) did not foresee auditors and regulators tolerating: companies were allowed to publish metrics with the names as ESRS/SFDR metrics but with different definitions, even without necessarily highlighting that fact.

One metric where this happened significantly was for non-recycled waste.

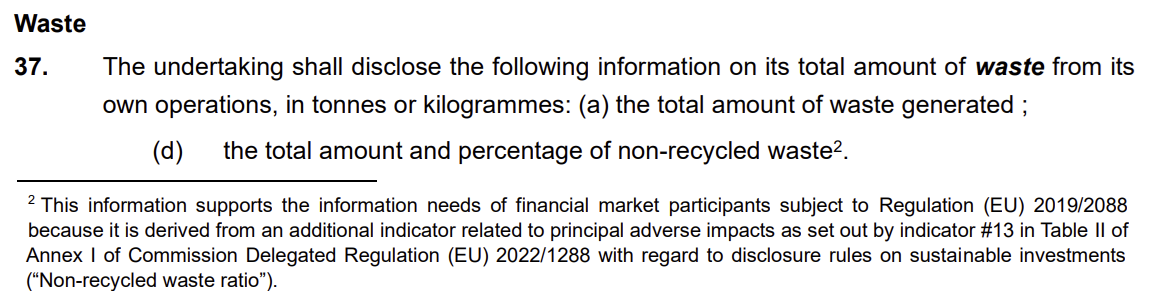

The paragraph in the sector-agnostic ESRS that defines and requires the disclosure of non-recycled waste

The simple definition of non-recycled waste in the SFDR

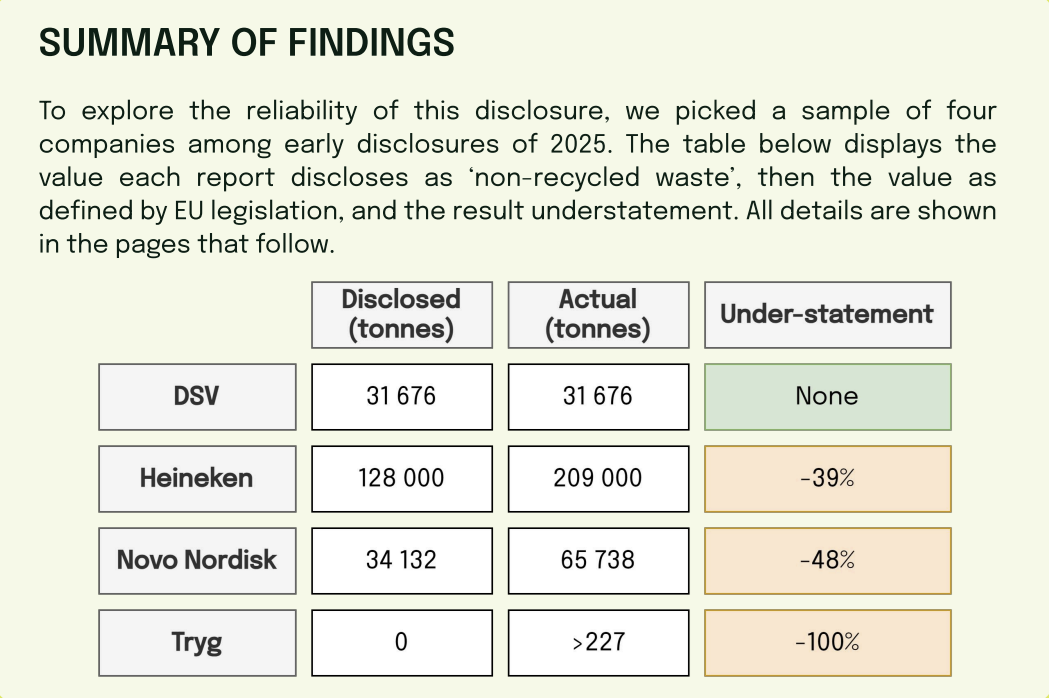

In 2025, I sampled a few companies that disclosed a mass or percentage metric named ‘non-recycled waste’. As the ESRS also requires a breakdown of waste according to its destination, I was able to manually recalculate the non-recycled waste according to the proper definition, i.e. the share of waste that is not recycled.

This was the outcome:

Out of four companies, only one used the proper definition, while the other three largely understated their non-recycled waste

The first year of application of a new standard requires leniency. Perfection was not expected.

Still, it was important to carefully watch reports, and to make a note of what needed to be improved. Otherwise, improvements in the following years become impossible.

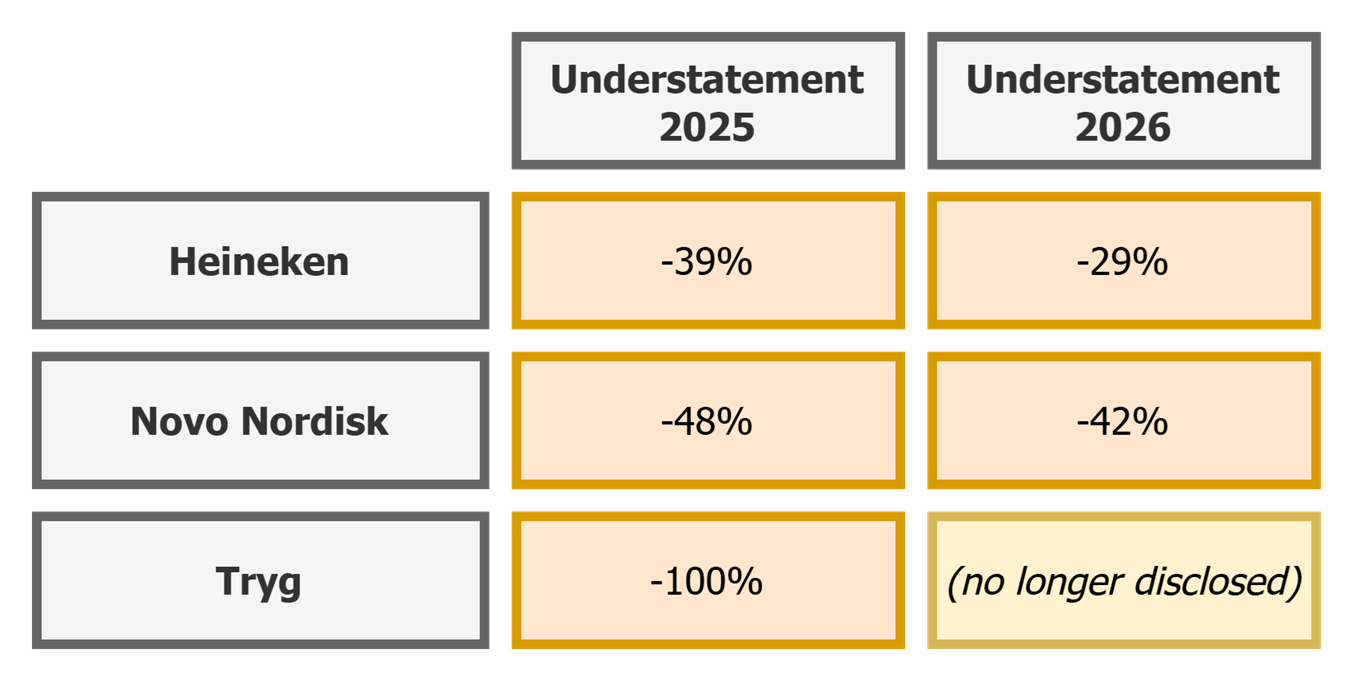

Non-recycled waste, year 2

And so, with the second wave of reports, let us have a look at the reports of the three companies that made understatements last year to see whether and how they improved.

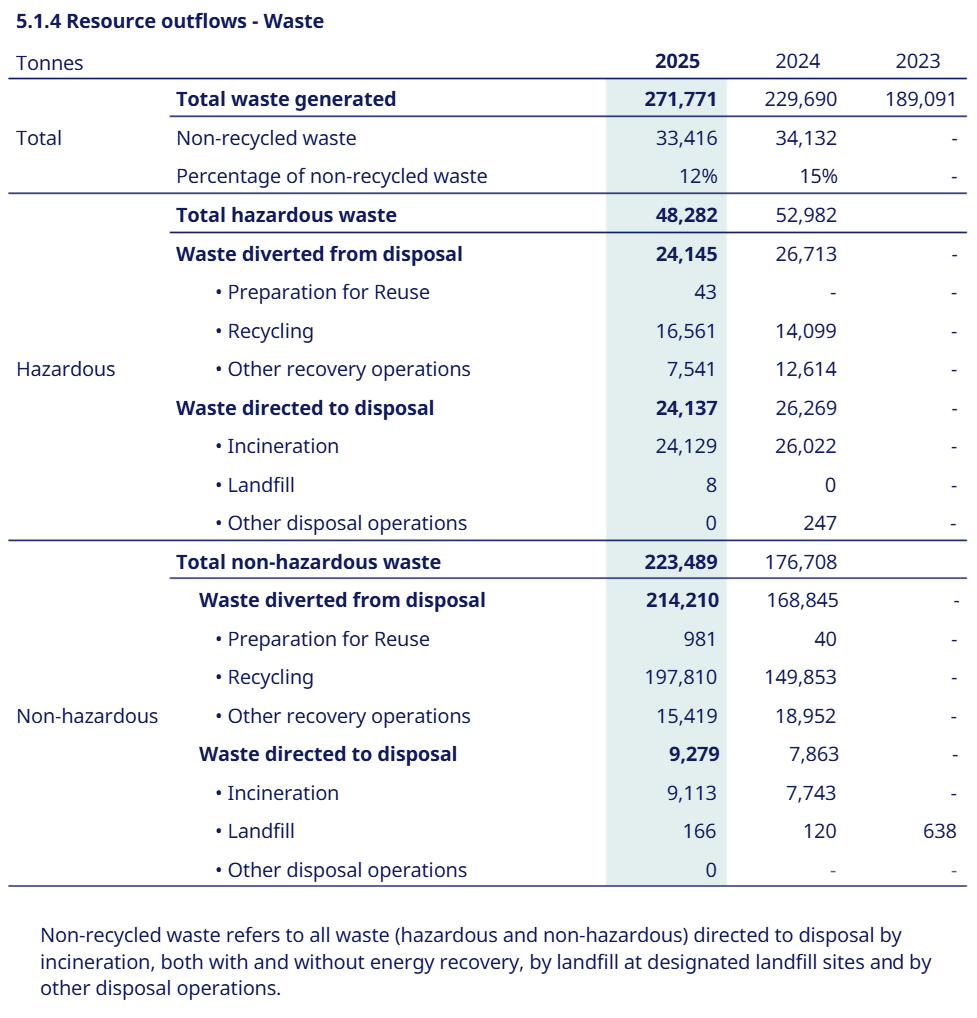

Heineken

In their 2026 publication, Heineken simply adopts exactly the same disclosure as in 2025. The metric it names ‘non-recycled waste’ excludes not only recycled waste, but also waste prepared for reuse.

As a consequence, there is this year again an understatement. With the actual non-recycled waste at 209 kt, Heineken again makes an understatement this year, by 29%.

Novo Nordisk

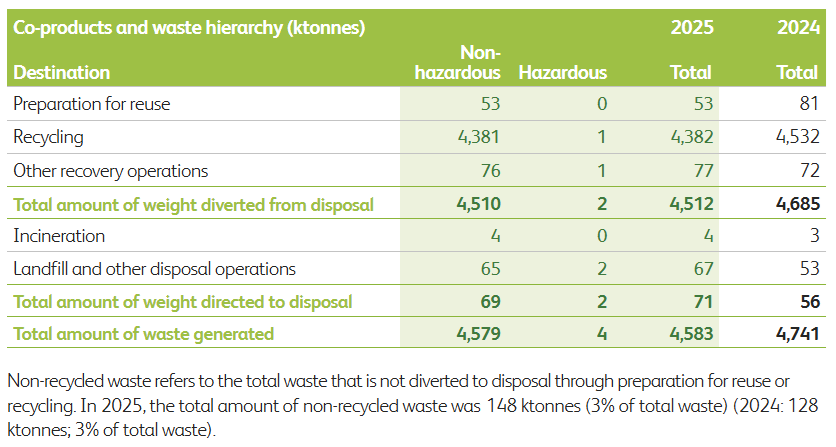

In their 2026 publication, Novo Nordisk has changed its presentation slightly, but the figures themselves are the same, and in particular, Novo Nordisk keeps its ‘non-recycled waste’ metric, with the same definition as last year, i.e. inconsistent with SFDR.

We can also infer from the accounting policy that the presented breakdown itself is not consistent with the ESRS:

the figure disclosed for ‘non-recycled waste’ is equal to ‘Waste directed to disposal’ (hazardous plus non-hazardous)

the accounting policy tells us this figure includes waste used for energy recovery

the ESRS make it clear that energy recovery is to be included in ‘other recovery operations’, in waste diverted from disposal.

At any rate, as a result, Novo Nordisk keeps understating their non-recycled waste, this year by 42%.

Tryg

Even as waste management remains an ‘operational priority’, Tryg assesses that resource outflow metrics being part of SFDR does not make that information material and chose not to disclose the information in 2026.

Summarised comparison

This is not a very encouraging comparison; the only company that changed its disclosure removed it.

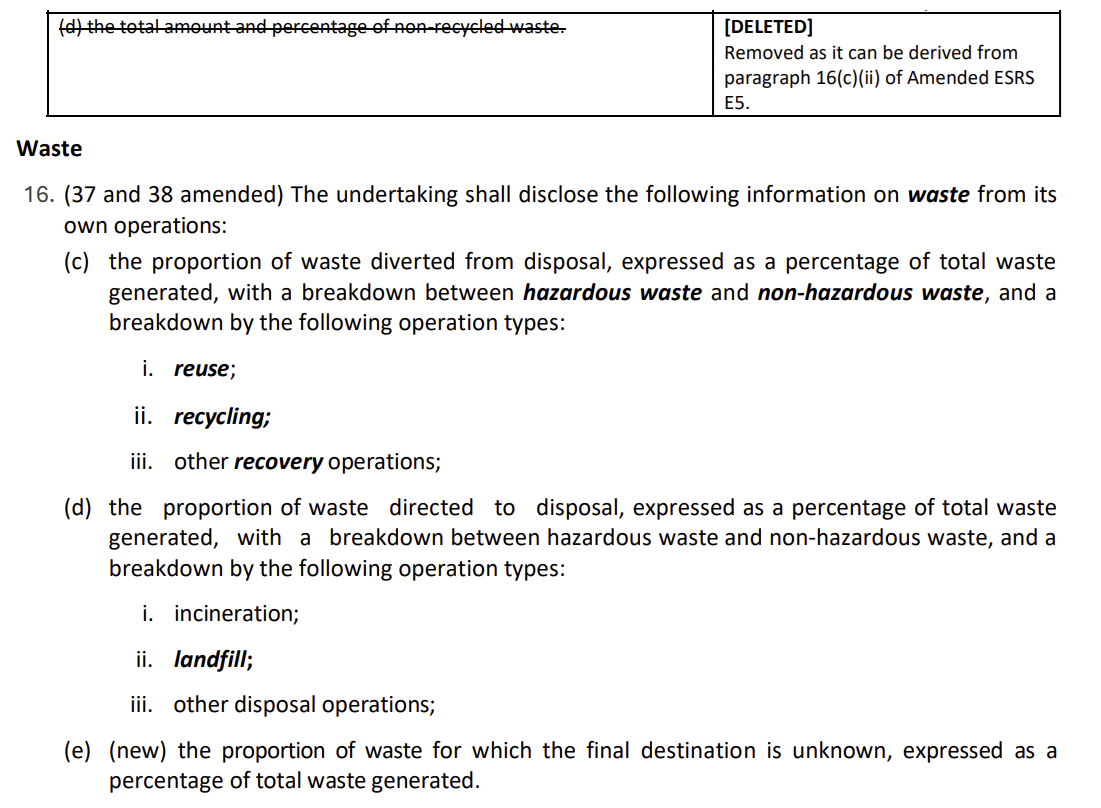

Non-recycled waste, amended ESRS

In 2026, the same requirements apply as in 2025 for both the ESRS and the SFDR. Of course, as the reader will probably be aware of if involved with sustainability, many amendments have been discussed that mostly aim at ‘simplifying’ both documents.

The following applied for non-recycled waste:

The percentage of non-recycled waste no longer is a required metric, and the reference to SFDR is deleted. Instead, as the breakdown is still required, it is expected that users will still be able to compute their SFDR metric from the breakdown.

The purpose of the change is probably really just to make the ESRS text shorter. One may think removing the percentage and relying to the breakdown could promote consistency, since users would be more likely to compute the correct percentage from the breakdown.

Unfortunately:

The removal of the reference to SFDR is a pity in itself, as preparers lose a hint that this metric is particularly important. How did we go from draft ESRS where consistency was required, to the first ESRS where it was only encouraged, to revised ESRS where consistency is considered to be superfluous?

There will not be much preventing companies from publishing a ‘percentage of non-recycled waste’ with a definition different from SFDR. Even more so now that the metric no longer is an ESRS metric in itself; it will be harder for reviewers and regulators to argue against the practice.

If enforcement remains as weak as it has been in the first two years, I believe it is likely that the trend will continue, where the CSRD will fail to accomplish its purpose of providing the market and other stakeholders with the data necessary to operate the EU’s sustainable policies.